As per the above table, it can be inferred that by the time appointment of Mr Ranveet Gill was made, the banking company was running in huge loses and financial stability was crippling. Yes Bank initiated a series of equity funding rounds but failed in materialising any deal for the infusion of capital. In this matter, RBI also took the Bank and market-led revival route rather than a regulatory restructuring and granted ample opportunities and extensions to Yes Bank to secure such equity investments. Furthermore, in the meantime, the Banking Company was subject to a regular outflow of liquidity and coupling NPAs.

Hence, RBI stepped in by obtaining the Order of Moratorium with an order to supersede the Board of Yes Bank Ltd. RBI, on March 6 2020, to revive the operation of the Bank and maintain the trust of depositors, notified a draft scheme of reconstruction named “Yes Bank Ltd. Reconstruction Scheme, 2020”14. The draft scheme was approved by the Government of India and was enforced on March 13, 202015. The reconstruction scheme altered the MOA of Yes Bank Ltd., mainly the Capital Clause, increasing the Authorized Capital up to Rs. 62,00,00,00,000 (Rupees Six thousand two hundred crores only).

This alteration was effected by infusion of equity in Yes Bank by State Bank of India, resulting in fiscal stability of the Bank. Nevertheless, the principal criticism of the reconstructions scheme is the dealing of instruments qualifying as Additional Tier-1 Capital (AT1). An AT1 capital bond can be defined as an unsecured hybrid debt instrument with no fixed maturity period, i.e. they are perpetual bonds having no redemption date and carry a call option. The concept of AT1 bonds was introduced as per the Basel III norms after the 2008 global financial crisis to ensure the liquidity of banks.

As per the Clause 6 of the Draft Reconstruction Scheme, the RBI proposed that on and from the appointed date from which the scheme comes into force, all the AT1 instruments issued by Yes Bank shall be written off from the books which shall result into wiping out of investments made in these instruments by Mutual Funds, financial institutions and pension funds. This treatment of AT1 instruments is challenged in the Bombay High Court by the Axis Trustee Services on the ground that preference given to equity of AT1 instruments in against global best practices and benefits the promoters of Yes Bank Ltd. over the bondholders’.

Although, Yes Bank is not a Domestically Systematically Important Bank (D-SIB) as identified by the RBI, however, the size of its balance sheet is the reason that RBI is taking all the necessary steps for its revival. The drastic action taken by RBI’s was a temporary yet necessary measure to safeguard the depositor’s interest and maintain the confidence and stability of the financial system. As the approved reconstruction scheme constitutes a new Board of Directorship appointing former CFO of SBI, Mr. Prashant Kumar as the CEO and MD, the intention should be of restarting the operations of the Bank focused on the retail banking.

The approved capital restructuring was achieved by SBI acquiring 49% of the shareholding of the Yes Bank. As per the approved scheme, the holding of SBI in Yes Bank’s capital shall not be less than 26% before completion of 3 years. The approved scheme also mandates a lock-in period of 3 years for the existing shareholders having 100 or more shares. This retrospective prohibition is an unprecedented step primarily affecting the minority shareholders and requires further regulatory clarifications from the government.

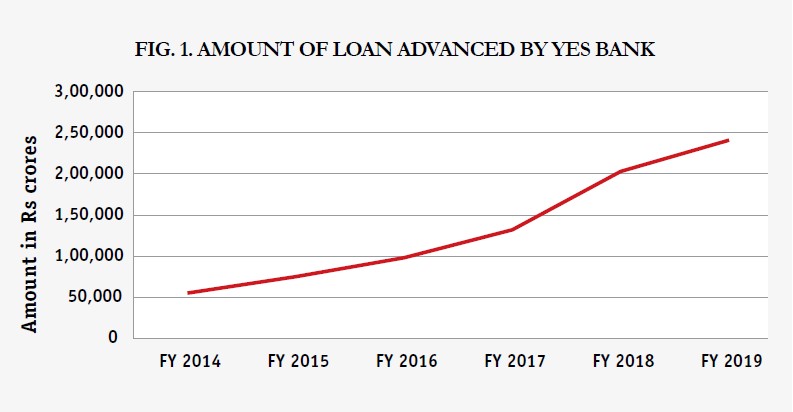

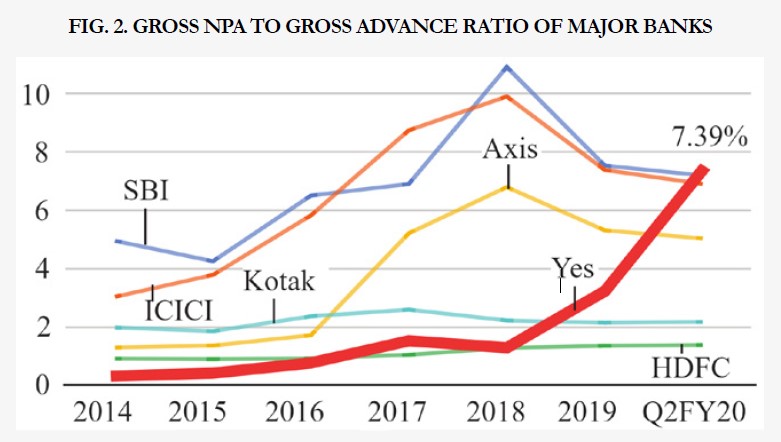

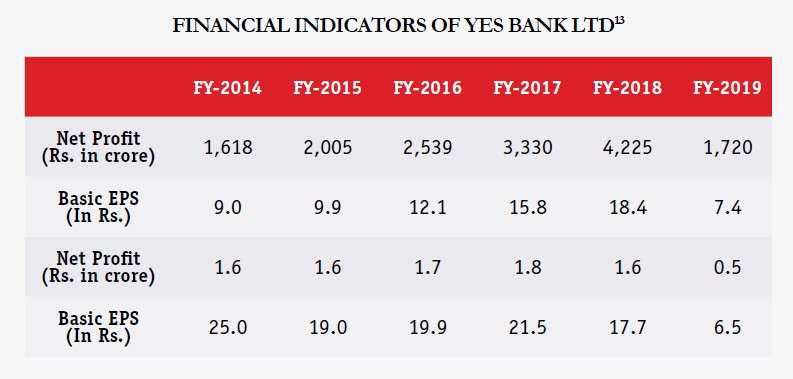

Although Rana Kapoor was arrested on March 7, 2020, by Directorate of Enforcement and is charged on the grounds of financial mismanagement and irregularities, the Yes Bank fiasco highlights the cracks in existing banking regulations. The current position of once India’s fourth-largest private Bank and the Punjab & Maharashtra Co-operative Bank Ltd. (PMC Bank) raises severe flaws and lacunae in the compliance framework in the Indian Banking sector. The crisis raises allegations against the compliance monitoring by RBI as it failed to notice the jump of 35% in loan granted by Yes Bank in a single year and failed to react promptly when the Bank incurred massive loss in Q1 of 2019.

It highlights the need for efficient and a permanent framework for dealing with such emergencies. This can include the establishment of a fast track resolution mechanism for banks which may be introduced with the introduction of the Financial Resolution and Deposit Insurance (FRDI) Bill. Another step that can be undertaken is carrying out Asset Quality Review (AQR), a clean-up exercise as done by RBI in 2015. The Indian banking sector needs systematic reforms as it is facing an NPA crisis as highlighted by Yes Bank case.