or

We are aware of the concept of Copyright which can be defined in a statement as ‘Rights of the owner of the original work to reproduce, distribute, communicate, translate, perform, broadcast, adaption into other forms and assign/ license all these rights to any third party.’ These are generally termed as exclusive rights of the copyright holder and are only available for exercise by the copyright holder or by any agent or third party who is expressly authorized to do so by the copyright holder.

In similar connotation, we usually come across the term rights of owner of ‘Copyrighted Product’ which is generally confused with the term “rights of owner of Copyright”. The confusion is obvious since these terms are closely associated with each other and a clarity on these concepts are not generally available in the public domain.

In view of the above, this article will focus on an attempt to clarify the terms ‘Copyright’ and ‘Copyrighted Product’, and further will explore the exclusive rights and applicability of fair use, with respect to the rights of the owner of Copyright and owner of the Copyrighted Product.

The confusion between the Copyright and Copyrighted Products, is the prime reason behind lack of awareness about the actual rights of these owners. The author believes that first step towards better understanding of these terms is to understand the rights of the owners of such works. Therefore, let us make an effort to understand the rights available to these owners as under:

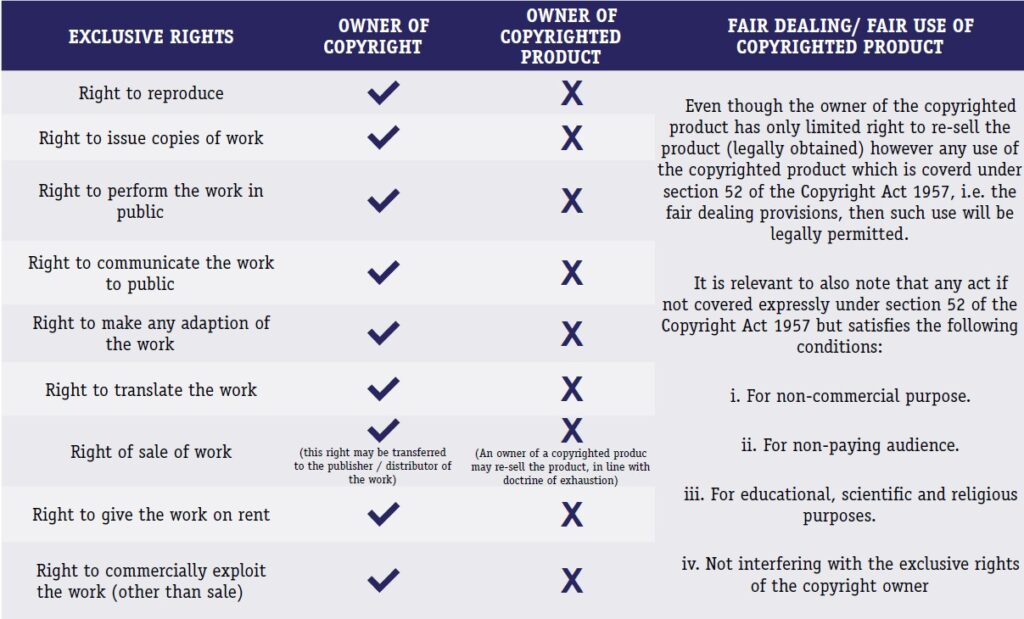

The reference to the above table clearly shows that owner of the copyright enjoys much broader and detailed exclusive rights as against the rights available with the owner of the copyrighted product. The distinctions of these concepts are most crucial in order to determine the extent of rights available with these owners. With the above table clearly defining the rights, let us discuss the exercise of rights by owner of the copyright:

The above understanding gives us a clarity that the owner of the Copyright and owner of the Copyrighted Product are different and have vested with separate set of rights.

The rights of the copyright owner is created as soon as the work is created whereas the rights of owner of the copyrighted product, comes into play, as soon as the transaction or purchase of the product is completed. The rights of copyright owner has more exclusive value pursuant to the nature of association the owner has with his copyright. The copyright owner, becomes the owner by virtue of being the creator of the original work,2 and is eligible to take action against infringement in light of unauthorized use or substantial copying, of his copyright.

As the copyrighted product owner has limited right to sell and rent the lawfully obtained copy of the work, therefore the concept of originality and substantial copying does not come into play for these owners. The owner of copyrighted product has limited rights and therefore limited power to exploit their work. With this we have now addressed one of the major conflicts in terms of rights for ‘Copyright’ and ‘Copyrighted Product’, and now let us look into the practical difficulties addressed and concluded by the various tribunals and courts through the course of their judgement.

Due to the confusion over these terms, ‘Copyright’ and ‘Copyrighted Product’, there has been various issues that have cropped up due to commercial use of the copyrighted product, through sale and under the fair use. However, such use of copyrighted product has raised conflicts with the rights of the copyright owner and various tribunals have discussed the issues and provided their viewpoint:

In the landmark case of Tata Consultancy Services Private Limited v. State of Andhra Pradesh,4 the Hon’ble Supreme Court held that “A software programme may consist of various commands which enable the computer to perform a designated task. The copyright in that programme may remain with the originator of the programme. But the moment copies are made and marketed, it becomes goods which are susceptible to sale tax. Even intellectual property, once it is put on to a media, whether it be in the form of books or canvas (in case of painting), or computer discs or cassettes and marketed would become good. We see no difference between a sale of software programme on a CD/ floppy disc from a sale of music on a cassette/ CD or a sale of a film on a video cassette/ CD. In all such cases, the intellectual property has been incorporated on a media for purposes of transfer. Sale is not just of the media which by itself has a very little value. The software and the media cannot be spilt up. What the buyer purchases and pay for is not the disc or the CD. As in the case of paintings or books or music or films the buyer is purchasing the intellectual property and not the media i.e. the paper or cassette or disc or CD. Thus, a transaction of sale of computer software is clearly sale of goods within the meaning of the term as defined in the said Act.”

The Hon’ble Supreme Court vide the above judgement has clarified that copyright when made into a media then such media is a ‘Copyrighted Product’ bearing the ‘Copyright’. Therefore, when any transaction with respect to the copyrighted product is made then any right which can be exercised is only with respect to Copyrighted Product and not with respect to the Copyright inside the Copyrighted product. This is an important clarification by the Hon’ble Supreme Court in order to make a clear distinction about the nature of transaction that occurs between the parties when the work in question is a ‘Copyright’ and when it is ‘Copyrighted Product’.

One of the situations which has time and again become a point of concern is the question that whether the payment made towards supply of the copyrighted product for mere use of the product amounts to ‘Royalty’. This has been a major concern for the Income Tax authorities, for determining whether payment received by the non-resident entities constitutes business profit or whether such payment amounts to transfer of copyright and therefore chargeable as ‘Royalty’.

In Ddit (It)-2(1), Mumbai vs M/S. Reliance Infocomm Ltd., held that the consideration paid by the assessee to the suppliers for acquiring copy of software was not for the ‘use of copyright or transfer of right to use of copyright’ the payment was made for the ‘copyrighted article’ and that the payments made by the assessee to the vendors of software cannot be taxed as royalty.

Further, the Hon’ble Delhi High Court in DIT v. Infrasoft Ltd., held that “The license granted to the licensee permitting him to download the computer program and storing it in the computer for his own use was only incidental to the facility extended to the licensee to make use of the copyrighted product for his internal business purposes. The said process was necessary to make the program functional and to have access to it and is qualitatively different from the right contempt related by the said provision because it is only integral to the use of copyrighted product. The right to make a backup copy purely as a temporary protection against loss, destruction or damage has been held by Delhi High Court in Nokia Networks OY (supra) is not amounting to acquiring a copyright in the software.”

In light of the above discussion, it can be concluded that when a person buys a copyrighted product then the only transfer that happens is the right to use the copyrighted product. Since there is no transfer of the copyright, therefore the question of payment amounting as ‘royalty’ does not arise. Various decisions have been observed from the tribunals and courts that has held that such payments cannot be treated as royalty under the Income Tax Act 1961. Similarly payment made for obtaining a license is also not in the nature of ‘royalty’.

When a copyrighted product is lawfully obtained by a person/ entity then use of such copyrighted product for the benefit of the person/ entity is protected under the Indian Copyright Act 1957. The use of copyrighted product by the owner of such product is protected as fair dealing under the Copyright Act 1957. India also acknowledge the acts as “Fair Use” when an act performed is beyond the scope of the already mentioned situations in section 52 of the Act.

It is relevant to identify the difference of fair use and fair dealing, in order to maintain clarity of these terms used. Both the terms “fair use” and “fair dealing” have different meaning when it comes to application of these terms in enforcement of the provision. When we talk about “Fair Dealing”, it essentially means certain specific acts recognized by the domestic laws which if done for the specific purpose as recognized, then the use of copyright for such recognized act will not be an infringement. On the other hand, the term “Fair Use” is used in domestic legislations where the criteria or factors are clearly mentioned, which if satisfied by an act, will not be an infringement of the copyright.

In a brief, it can be concluded that when an act by owner of the copyrighted work is either covered by the circumstances mentioned in section 52 of the Act, or if such act satisfies the following conditions:

When an act is performed in furtherance to fair dealing/ fair use, then the act so done is protected under the Copyright law.

In view of the above discussion, it is concluded that ‘Copyright’ and ‘Copyrighted Product’ are separate concepts and have separate set of rights vested with the owners of these rights. Copyright being associated with the copyrighted content gives the owner set of exclusive rights expressly mentioned under section 14 of the Copyright Act 1957. Whereas the Copyrighted Product is a media in which the copyrighted content are covered or made into, for easy sale or marketing of the product.

By establishing the difference, it is further ascertained that Copyrighted Product is mere media and by virtue of any transaction in furtherance to the buying of the Copyrighted Product only transfers the right over the Copyrighted Product and not with respect to the copyright in the product. In line of this and to address the contrary view point, it is also clarified that any act done, in furtherance to safeguard the lawfully obtained copyrighted product and in conformity with the provisions of section 52 of the Copyright Act 1957, then such acts are protected under the ambit of fair use by the owner of the Copyrighted Product.

An example to this regard can be ‘ABC, copyright Owner, developed an original software for maintaining a dashboard by using unique filters to help management of the office functions and maintaining records. ABC decides to convert the software into a media and sell the product for market use (the media, in form of CD or DVD or floppy or pen drive, become the copyrighted product). XYZ purchases the software from ABC (XYZ becomes the owner of the copyrighted product). Now an act of reproduction, storage, internal use, access given to the office staff for maintaining office functions and records, performed by XYZ by using the software will be protected under the provisions of section 52 of the Copyright Act 1957.

In light of the above example it is pertinent to note that any act by the owner of the Copyrighted Product which if in conflict with the exclusive right of the copyright owner, will be an infringement of the exclusive rights of the copyright owner unless a fair use or fair dealing defence can be justified by the owner of the copyrighted product.

Tags: S.S. Rana & Co

Lucy Rana is a Partner at S.S. Rana & Co. Her practice is focused on Intellectual Property and Corporate Law with emphasis on luxury goods, F&B, FMCG, hospitality, E-commerce, Information technology, automobile, sports and fitness, media and entertainment and the gaming industry industries. Lucy assists both multinational corporations and grassroot startups on all aspects of brand development from inception through international and national expansion and beyond.

Meril Mathew Joy is an Associate Advocate at S.S. Rana & Co. He is a part of Trademarks & Copyright Department and mainly focuses on advisory and prosecution of Trademarks and Copyright. Prior to joining S.S. Rana & Co., Meril worked with the Indian Copyright Office as an Examiner of Copyrights responsible for scrutinizing the copyright applications and copyrightability of a work. Pursuant to his experience with the Copyright Office, he has developed an understanding on the classes of work and their standards for evaluating the copyright-ability of the work. Further, his experience also expands to assisting the Learned Registrar of Copyrights in Copyright hearings.

Lex Witness Bureau

Lex Witness Bureau

Advertisement

For over 10 years, since its inception in 2009 as a monthly, Lex Witness has become India’s most credible platform for the legal luminaries to opine, comment and share their views. more...

Connect Us:

The Grand Masters - A Corporate Counsel Legal Best Practices Summit Series

www.grandmasters.in | 8 Years & Counting

The Real Estate & Construction Legal Summit

www.rcls.in | 8 Years & Counting

The Information Technology Legal Summit

www.itlegalsummit.com | 8 Years & Counting

The Banking & Finance Legal Summit

www.bfls.in | 8 Years & Counting

The Media, Advertising and Entertainment Legal Summit

www.maels.in | 8 Years & Counting

The Pharma Legal & Compliance Summit

www.plcs.co.in | 8 Years & Counting

We at Lex Witness strategically assist firms in reaching out to the relevant audience sets through various knowledge sharing initiatives. Here are some more info decks for you to know us better.

Copyright © 2020 Lex Witness - India's 1st Magazine on Legal & Corporate Affairs Rights of Admission Reserved